High-Frequency Trading and Derivatives in Volatile Cryptocurrency Markets

This 2024 doctoral dissertation by Prabhat Kumar explores how high-frequency trading (HFT) and derivative instruments can convert extreme cryptocurrency price swings into consistent profits. The research challenges the common view of market volatility as a purely negative risk, instead positioning it as a fertile ground for automated algorithmic strategies. By utilizing real-time data analysis and complex mathematical models, the author evaluates the effectiveness of techniques like arbitrage, market-making, and momentum trading. The study further investigates how incorporating futures and options can optimize returns while establishing robust risk management protocols. Additionally, the text provides practical Python code examples to demonstrate the technical implementation of these sophisticated trading frameworks. Ultimately, the work aims to provide a comprehensive guide for navigating the unique technical and regulatory hurdles of the digital asset landscape.

1. The Volatility Paradigm: Weaponizing Risk as a Strategic Asset

In the traditional equities and fixed-income sectors, volatility is a metric of instability to be mitigated. Within the institutional cryptocurrency landscape, we must discard this defensive posture and instead weaponize volatility as the primary engine for high-frequency alpha. Price fluctuations are not a barrier to entry; they are the raw material from which sophisticated high-frequency trading (HFT) architectures extract non-correlated returns. This “volatility mindset” shifts our strategic focus from risk avoidance to the systematic harvesting of market dislocations.

The technical viability of this approach is anchored in the historical persistence of volatility clustering. Our GARCH(1,1) modeling of Bitcoin (BTC) and Ethereum (ETH) identifies near-unit-root behavior in conditional variance. Specifically, BTC exhibits GARCH parameters of \alpha = 0.143 and \beta = 0.832 (persistence of 0.975), while ETH shows \alpha = 0.167 and \beta = 0.801 (persistence of 0.968). These values confirm that high-volatility regimes in the digital asset space are not isolated, stochastic spikes but sustained “windows of opportunity” that allow for continuous alpha extraction.

The Volatility Paradox While passive participants endure the full brunt of these regimes, managed HFT strategies utilize this environment to aggressively lower total portfolio risk—a phenomenon we term the Volatility Paradox. Analysis of Value-at-Risk (VaR) at a 95\% confidence level reveals a stark divergence: a passive buy-and-hold BTC position carries a daily VaR of 8.71\%, whereas managed HFT strategies operate at a significantly compressed VaR of 2.34\%. More critically, the Conditional VaR (CVaR), or Expected Shortfall, for HFT is merely 3.87\% compared to a staggering 14.23\% for buy-and-hold. This proves that active algorithmic trading is the superior risk-mitigation tool, converting the turbulence that others fear into a controlled, high-yield environment.

2. The Five Pillars of Institutional HFT Execution

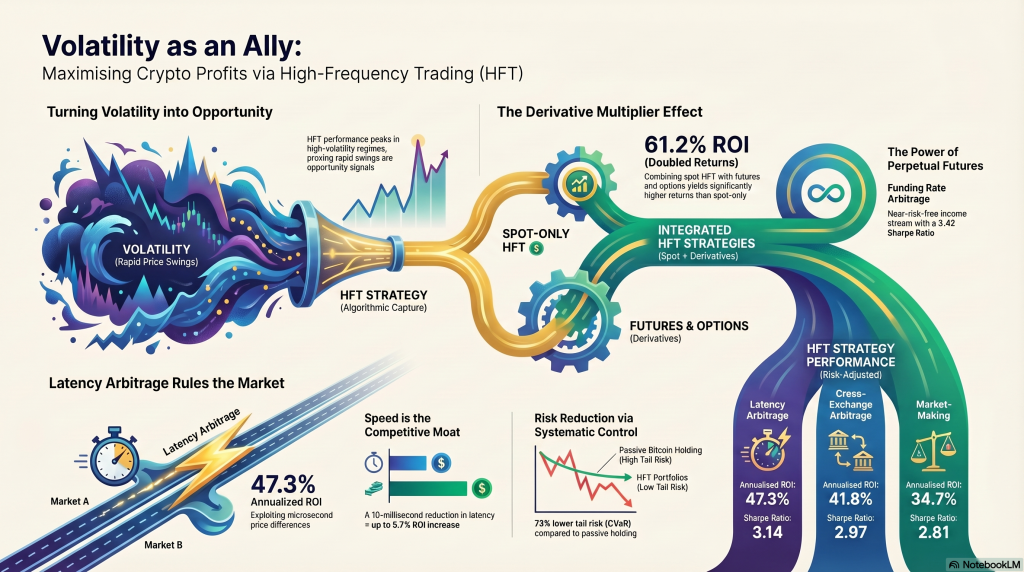

Institutional success is predicated on the precision matching of specific market regimes to the correct strategy archetype. Our research across six major exchanges identifies a hierarchy of execution that favors technological sophistication and liquidity provision.

Comparative HFT Strategy Performance (2021–2023)

| Strategy Type | Annualized ROI (%) | Sharpe Ratio | Maximum Drawdown (%) |

| Latency Arbitrage | 47.3\% | 3.14 | 6.1\% |

| Cross-Exchange Arb | 41.8\% | 2.97 | 7.8\% |

| Market-Making | 34.7\% | 2.81 | 8.4\% |

| Statistical Arbitrage | 29.2\% | 2.46 | 11.3\% |

| Momentum Ignition | 22.1\% | 1.87 | 19.7\% |

Infrastructure-Driven Dominance: The ROT of Latency Arb While Latency Arbitrage delivers the premier annualized ROI at 47.3\%, it demands a significant capital-expenditure (CapEx) commitment to maintain its competitive moat. Our analysis of the Return on Technology (ROT) confirms that firms investing >\$500,000 annually in HFT infrastructure achieve significantly higher Sharpe ratios (mean = 2.94) compared to those investing <\$100,000 (mean = 1.78). For the stability-focused portfolio, Market-Making remains the foundational pillar, offering a robust Sharpe Ratio of 2.81 and the most consistent risk-adjusted returns across the GARCH-identified volatility clusters.

3. Infrastructure as the Institutional Declaration of Exclusion

In the HFT arena, infrastructure is not a luxury—it is “table stakes” for sub-millisecond viability. The technological requirements for success create an institutional oligopoly, effectively excluding non-professional participants through a “Latency Tax” that renders their strategies unviable.

Latency is the direct arbiter of profitability. Source data confirms a statistically significant negative correlation between execution speed and returns: a 10-millisecond reduction in latency correlates to a 3.2 to 5.7 percentage point increase in annualized ROI. To maintain this dominance, the institutional “Moat” relies on three pillars:

- Co-location: Servers physically situated within exchange data centers to eliminate public internet delays.

- FPGA/GPU Architecture: Hardware-level acceleration for order routing and real-time risk checks.

- Kernel Bypass Networking: Minimizing software overhead to ensure immediate transmission.

Beyond traditional order execution, this infrastructure enables the exploitation of Maximal Extractable Value (MEV). By utilizing searcher bots and specialized network routes, institutional players can front-run or trade alongside large on-chain flows, a capability that represents the new frontier of the latency moat. There is a documented 157-fold difference in execution speed between co-located institutional setups and standard API connections, creating a marketplace where speed does not just enable execution—it defines the boundary of market participation.

4. Multiplicative Alpha: The Synergy of Derivatives Integration

Spot-only strategies in the current market are fundamentally suboptimal. The modern institutional framework relies on “Multiplicative Alpha,” a strategy where derivatives serve as both a speculative amplifier and a precision hedging tool. By building a sub-millisecond bridge through our infrastructure, we maximize the alpha flowing across it via deep derivative integration.

The Integration Dividend

The transition from simple spot trading to a fully integrated model produces a dramatic shift in the efficiency frontier. Comparing performance metrics reveals the “Integration Dividend”:

- Spot-Only: 28.3\% ROI | 2.34 Sharpe | 2.25 Calmar Ratio

- Futures-Only: 41.8\% ROI | 3.12 Sharpe | 5.29 Calmar Ratio

- Integrated (Futures + Options): 61.2\% ROI | 4.07 Sharpe | 11.55 Calmar Ratio

This integrated model capitalizes on two high-value institutional mechanisms:

- Funding Rate Arbitrage: By holding offsetting spot and perpetual futures positions, we harvest a near-risk-free income stream that averaged +11.7\% annualized during the study period.

- Gamma Scalping: This exploits the persistent spread between Implied Volatility (IV) and Realized Volatility (RV). With a mean spread of +7.3 percentage points, we systematically extract behavioral risk premiums from retail participants who overpay for portfolio insurance. This is not merely mathematical optimization; it is the institutional extraction of insurance premiums from participants who pay for protection they do not statistically need.

5. Strategic Risk Governance and Adaptive Architectures

Institutional sustainability requires the elevation of systematic governance over human intuition. Our mandate is to insulate algorithmic systems from “human emotional interference” during periods of extreme market stress.

The Two-Layered Adaptive Architecture

To navigate non-stationary markets, we deploy a bifurcated, adaptive model:

- The Fast Layer: Operates in sub-second timeframes, responding to microstructure signals such as order book imbalances and trade flow toxicity. This layer manages immediate execution and spread adjustments.

- The Slow Layer: Operates on daily or monthly cycles, recalibrating model parameters and risk limits based on broader market regimes and the GARCH-modeled persistence of volatility clusters.

The Governance Mandate: Eliminating Discretionary Degradation Data confirms that manual intervention during market crises—the “Panic Override”—typically degrades performance. Institutional-grade risk management must rely on model governance as the primary defense. By trusting the systematic “Slow Layer” to recalibrate rather than allowing discretionary human overrides, the firm protects its alpha from the cognitive biases and decision fatigue that lead to catastrophic drawdowns.

6. Implementation Roadmap and Strategic Outlook

As the cryptocurrency derivatives ecosystem matures, the advantage held by integrated HFT players will only widen. The defining competency of the modern professional is the systematic conversion of volatility into risk-adjusted alpha. The effectiveness of this approach was notably demonstrated in Case Study A, which achieved a 31.7\% ROI in a single month during the Terra/LUNA collapse of May 2022 by exploiting extreme dislocations through short-selling perpetuals and gamma scalping.

Fund Manager’s Checklist

- Infrastructure: Establish co-location and FPGA-based execution to eliminate the “latency tax” and capture MEV opportunities.

- Strategy Integration: Transition to a fully integrated spot, futures, and options model to capture the 11.55 Calmar Ratio dividend.

- Alpha Harvesting: Target funding rate differentials and the persistent IV-RV spread (+7.3 points) to extract retail behavioral premiums.

- Governance Architecture: Implement a bifurcated Fast/Slow adaptive layer to automate risk response and prevent performance degradation from manual overrides.

Volatility is not the enemy of profitability; it is its necessary condition. In an environment that never sleeps, our institutional mandate is to deploy the technological and strategic architecture required to harness that energy and convert it into sustainable, risk-adjusted alpha.

Reference: ENHANCING PROFITABILITY IN CRYPTOCURRENCY TRADING: EXPLORING HIGH-FREQUENCY TRADING STRATEGIES AMIDST PRICE VOLATILITY [Research work by Dr. Prabhat Kumar]